Further big improvements in America’s labor market statistics at the beginning of this year – with net new jobs creation climbing by almost half a million (+473,000) and the unemployment rate falling to a tight 4.7% − have convinced many analysts that the Federal Reserve will be acting quite aggressively in 2017 to hike interest rates. Where before there was an expectation that the federal funds rate would be lifted two or three times through December, by 25 basis points on each occasion (with 100 basis points equaling 1.00%), the consensus now is for an upward adjustment more frequently, either three or four times.

The Fed is probably hoping to attain, in easy-to-absorb stages over this year and next, a key policy-setting rate close to 3.00%. Nor are stock markets viewing such a prospect with anything like the same amount of dread as in the not so distant past. Share prices have been on a roll that has taken them to all-time highs.

Canada’s most recent employment report had a bottom line figure that wasn’t particularly outstanding (i.e., net new jobs of +15,000 in February), but included in the detail was an impressive increase in full-time staffing (+105,000), with most of the gain (+84,000) coming among what are termed ‘core-aged’ women (i.e., females 25-to-54 years of age).

While there was a largely offsetting decline (-90,000) in part-time work in Canada in February, it’s the creation of usually higher-paying and more stable 40-hour workweek or permanent positions that are looked on with more favor.

Also, Canada’s unemployment rate has now fallen to 6.6%, its best level since January 2008. After some tough economic slogging in 2015 and 2016, the Bank of Canada must be breathing a little easier.

Against the foregoing labor market backdrops in the U.S. and Canada, there are the following additional economic ‘nuggets’ to be gleaned from the latest government agency and private sector data releases. As I’m always fond of saying, the soil is rich and the crop abundant.

(1) In each of the three months following a quarter, the Bureau of Economic Analysis (BEA) calculates and publishes increasingly refined estimates of latest period-to-period gross domestic product (GDP) growth (or lack thereof). The first one is called a ‘preliminary’ estimate and then there are ‘second’ and ‘third’ estimates. For Q4 of 2016, the BEA’s ‘second’ estimate of quarter-to-quarter U.S. GDP growth, annualized, is +1.9%. That was a slowdown from Q3’s +3.5%, but it was better than Q2’s +1.4% or Q1’s +0.8%. The quarterly growth rates in 2015 had been: +2.0%, Q1; +2.6%, Q2; +2.0%, Q3; and +0.9%, Q4.

(2) For the full year, 2016, the BEA is now estimating that U.S. ‘real’ (i.e., inflation-adjusted) GDP growth (versus 2015) was +1.6%, which was a throwback to the pace of increase realized in 2013, +1.7%. In the two intervening years, the rise was a little faster, +2.6% in 2015 and +2.4% in 2014.

(3) During the past two years, personal consumption expenditures (PCE) in the national accounts, at +3.2% in 2015 and +2.7% in 2016, have exceeded the overall output improvement. Residential investment has also held up well, +11.7% in 2015 and +4.9% in 2016. But government spending has acted as a drag, net foreign trade (i.e., exports minus imports) has struggled to make progress and investment in non-residential structures has been disappointing, -4.4% in 2015 and -3.0% in 2016.

(4) Let’s provide some longer-term historical context for 2016’s +1.6% GDP growth rate. America’s average annual GDP increase throughout the ten years of the 1990s was, remarkably, twice as fast, +3.2%. The average annual increase throughout the 00s was a more restrained +1.8%. The 00s were laid low, however, by negative GDP performances in 2008 and 2009, -0.3% and -2.8% respectively. In the seven years since the Great Recession, 2010 through 2016, the average annual gain has been +2.1%.

(5) Canada’s quarterly GDP advances, annualized, throughout last year were: +2.8%, Q1; -1.2%, Q2; +3.6%, Q3; and +2.4%, Q4. The -1.2% in 2016’s Q2 was the third time there has been a quarter-to-quarter decline in Canada’s GDP since the Great Recession. While not judged by the technical experts to have been an official recession, because the weakness stayed minor, there were back-to-back drops in Q1 (-0.8%) and Q2 (-0.4%) of 2015.

(6) Canada’s full-year 2016 GDP step-up was +1.4%, slightly smaller than in the U.S. The historical record of Canada’s GDP changes has displayed less volatility than U.S. comparable figures. In fact, annual averages for Canada in the 90s (+2.4%), in the 00s (+2.1%), and during the latest seven years from 2010 on (+2.2%) have shown a high degree of consistency.

(7) By the fourth quarter of last year, the ‘current’ (i.e., not adjusted for inflation) dollar value of U.S. GDP was $18.9 trillion. Canada’s level was just above $2 trillion. Interestingly, there is a slightly more than 9-to-1 relationship between the two numbers. The population of the U.S. is nine times as large as Canada’s. (When comparing the two countries, most people use the mathematically simple 10-to-1 ‘rule of thumb’, even though it’s not strictly accurate.) But the $2 trillion for Canada’s GDP is in ‘loonies’ (i.e., the domestic currency). When the exchange rate differential is taken into account, Canada’s GDP is currently about 1.5 trillion in USD terms.

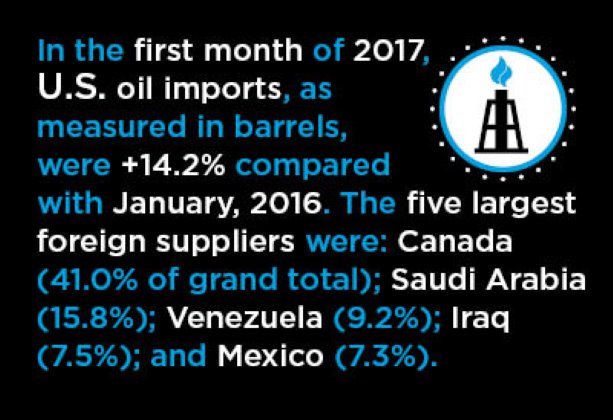

(8) In the first month of 2017, U.S. oil imports, as measured in barrels, were +14.2% compared with January, 2016. The five largest foreign suppliers were: Canada (41.0% of grand total); Saudi Arabia (15.8%); Venezuela (9.2%); Iraq (7.5%); and Mexico (7.3%). The year-over-year changes in barrels imported from those five countries were: Canada, +9.3%; Saudi Arabia, +8.9%; Venezuela, +17.7%; Iraq, +284.1%; and Mexico, -3.5%. Beyond those ‘big five’, some smaller-volume suppliers had exaggerated swings in their crude shipments to America: Nigeria, +166.0%; Brazil, +31.9%; Columbia, -31.6%; and Ecuador, -28.1%.

(9) Now that Saudi Arabia is no longer deliberately pumping out excess oil to keep the international price at a bargain-basement level, Canada’s energy-dependent provinces are reaping sizable revenue gains. Whereas the Canadian-dollar-volume of Saskatchewan’s energy exports was -54.4% in January of last year, they were an (exactly) inverted +54.4% in the first month of this year. For Newfoundland and Labrador, the shift has been from -30.5% to +45.9%. And for Alberta, by far the nation’s largest extractor of fossil fuels, from -28.6% to +25.5%.

(10) The Purchasing Managers’ Index (PMI) of the Institute of Supply Management (ISM) leapt 1.7 percentage points in February to 57.7% from 56.0% in January. The current reading is the highest since August 2014’s 57.9%. According to the ISM, when the PMI is above 50.0%, both the general economy and the manufacturing sub-sector are expanding. Above 43.3% but below 50.0%, the economy is still moving forward but manufacturing activity is slipping. Less than 43.3% and neither the economy nor manufacturing are making any headway. Based on the historical relationship between the PMI and national output, a reading of 57.7%, if extended over the entire year, would correspond with an outstanding GDP growth rate of +4.5%.

(11) Respondents to the most recent ISM survey were especially bullish on production and new orders, with expressed intentions to ramp up hiring as well. Deliveries from suppliers have become slower and the cost of inputs, especially commodities, is on an uptrend. These all signal a rosier outlook. They are also in keeping with a chirpier attitude being reflected in the Consumer Confidence Index (CCI) of the U.S. Conference Board. The CCI in February rose to 114.8 from an already strong 111.6 in January. The base for the index is 1985 equal to 100.0. (In 1985, consumer confidence was neither too ebullient nor too down-in-the-dumps.) Lately, the CCI has been at levels not seen in 15 years.

(12) Canada’s housing starts in February stayed above the 200,000-unit benchmark level for the third month in a row, plus they continued to maintain an upward progression. In steady stages, they have climbed from 188,000 units in November 2016 to a present perch of 210,000 units. But ongoing resilience in Canada’s homebuilding sector is old news. It’s the long-awaited improvement in the country’s foreign trade balance that is a greater cause for celebration. In January, for the first time in three years, there was a stringing together of three straight months of merchandise (i.e., trade in ‘goods’ as opposed to ‘services’) surpluses.

Recent Comments

comments for this post are closed